Senate committee approves bill to raise maximum interest rate on consumer loans

By Stephen Baldwin, RealWV

At the request of industry, senators in the Banking & Insurance Committee approved SB702 on Wednesday. The bill pertains to “setting new maximum annual interest rates for regulated consumer lenders on certain loans,” according to the introduction provided by Sen. Mike Azinger, R-Wood, chair of the committee.

Legal counsel for the committee described the purpose of the bill. “In effect the bill increased the allowable rate of finance on installment loans to 36% by removing a current tiered structure of 18, 21, and 27%.” She also said the new rates would apply to loans ranging from 6-120 months.

Sen. Jason Barrett. R-Berkely, asked if the purpose of the bill is to allow folks who wouldn’t normally qualify for credit to qualify by raising the interest rate?

“Yes,” answered Self Al-Zain, Vice President of Government Affairs for Lendmark Financial. “Today we have a 27% flat rate on anything between $3,500-$15,000. Lets say we can’t approve John at 27% because of his credit score and other credit factors. But he could qualify at 28%. He could go to an online lender but it would be a triple digit APR online.”

Al-Zain argued that by increasing the current maximum interest rate, it would allow his company to offer loans to more people by charging them a higher rate than they can currently, but a lower rate than those same customers would pay via an online lender. According to his testimony, online lenders are not regulated the same way as brick and mortar financial branches like Lendmark are, allowing them to charge customers triple-digit interest rates.

“If we can accept more of those people, that’s more people we can save from predatory loans.”

Lendmark Financial operates 13 branches across West Virginia. Nationally, they are a leading provider of consumer loans. In recent years, they’ve expanded their footprint across the United States. “We believe the Lendmark experience is underpinned by the level of empathy and trust our loan consultants build with customers in each branch, growing into genuine relationships that, in many cases, last beyond the life of the loan,” said Bret Hyler, President and Chief Operating Officer of Lendmark, when opening new branches in the south last year.

This move comes as delinquencies on household debt stand at their highest levels in a decade nationally. A new report issued by the Federal Reserve Bank of New York’s Center for Microeconomic Data on February 10 noted that “total household debt increased by $191 billion, 1.0%, in Q4 2025, to $18.8 trillion.” The report also stated, “Transitions into serious delinquency ticked up for credit card balances, mortgages, and student loans.”

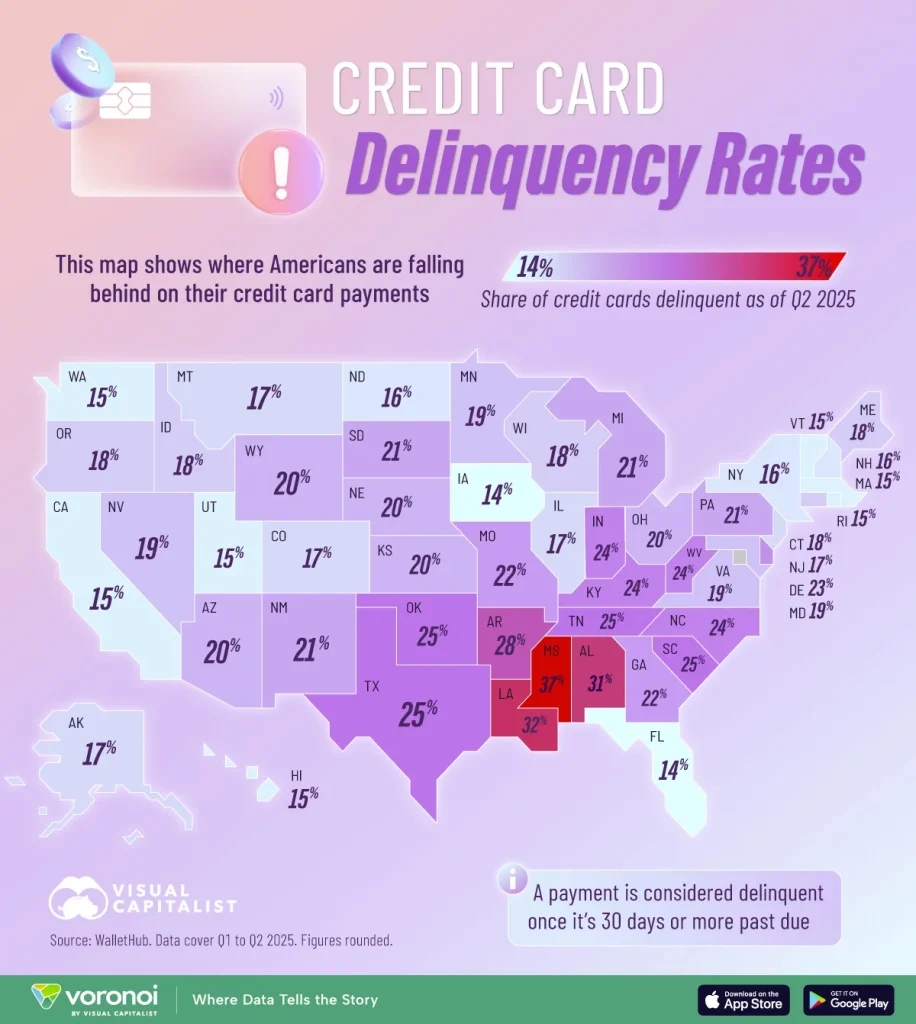

On a state level, West Virginia has a 24% delinquency rate for credit card debt, one of the highest in the nation, according to Visual Capitalist.

SB702 now heads to the Senate Finance Committee for further consideration.